Capital structure decisions

This article looks at the main ratios of investor interest and the impact of capital structure decisions on a company’s market value. Selecting the best possible capital structure is a crucial strategic decision. We also look at the effects of changing the capital structure by changing the cost of capital.

The capital structure decision

We have previously looked at the sources and costs of debt and equity financing. However, We now need to find out what debt and equity ratio an organization should use. Debt financing can create significant tax savings that can reduce the cost of capital and increase shareholder value. However, too much debt increases financial risk. Also, as a finance manager, you should keep in mind that the cost of debt is cheaper than the cost of equity.

Kd < Ke

The advantages of using debt finance

There are several advantages to selecting debt as a source of funding for a company.

- This is a cheaper source of finance due to the tax benefits obtains.

- The company assets secure debt, hence investors preferred.

- In a liquidation situation, debt holders are prioritized

- There is a lower issue cost.

- No immediate change in the controlling power of the company.

Disadvantages of debt

- Interest is payable even though the company is at a loss.

- Direct financial distress cost – higher interest payments, liquidation processes

- Indirect financial distress cost – higher costs from suppliers, loss of sales

- The company must make provision for the redemption of debt

- When the company obtains debt, financial risk also tends to increase.

The effect of capital structure on ratios/capital structure ratios

As the finance manager, when you are deciding on capital structure, it impacts several key ratios such as gearing, interest cover, and earnings per share.

Therefore, when the company is increasing its gearing level, financial risk tends to increase.

So, let’s deeply look at how the WACC will respond to the changes in the capital structure. When gearing is increasing, the WACC of the company tends to decrease because of the cheaper debt increasing. On the other hand, financial gearing is an attempt to quantify the degree of risk involved in holding equity shares in a company. When the company decided to increase it’s gearing level, the fixed interest portion that has to be paid for the fund providers will also increase.

Therefore, investors will face the volatility of their earnings (Dividends). As a result of that, the financial risk and the cost of equity also increases. Above all, this will tend to increase the WACC (Weighted Average Cost of Capital) of the company. So, looking at the above mentioned two aspects, one will increase the WACC, and the other will decreases the WACC. Therefore, the company must balance these two aspects.

Theories of capital structure

Two main theories attempt to explain the changes in capital structure on the cost of capital.

- Traditional Theory

- MM Theory

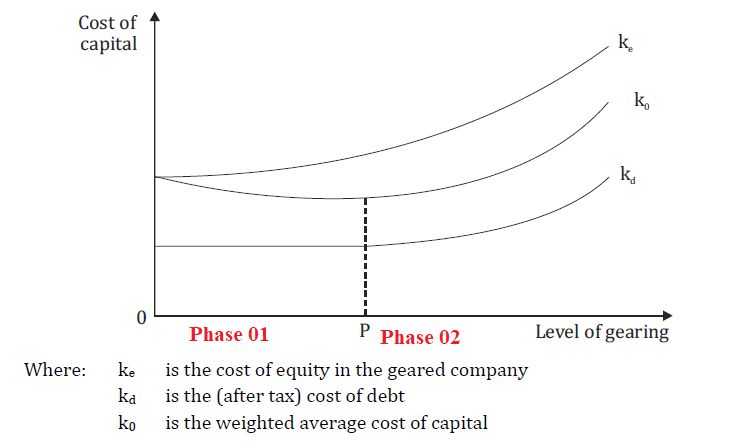

Traditional Theory

In traditional theory, when increasing the debt capacity of the company, WACC tends to decrease to some extent, and then again, it tends to increase as the debt further increases. The point where the WACC lowest is considered as the optimal capital structure for the company. As far as phase 1 is concerned, the benefit of cheaper debt is higher than the increasing financial risk. However, in phase 2 of the chart, the benefit of cheaper debt will tend to decrease.

The net operating income (Modigliani-Miller (MM)) view of WACC

In their 1958 theory, Modigliani and Miller (MM) proposed that the total market value of a company, in the absence of tax, will be determined only by two factors:

- The total earnings of the company

- The level of operating (business) risk attached to those earnings

Thus, Modigliani and Miller concluded that a company’s capital structure would not affect its overall value or WACC.

The assumption made for the net operating income approach.

- A perfect capital market exists

- No taxation involved

- Debt is a risk-free funding method

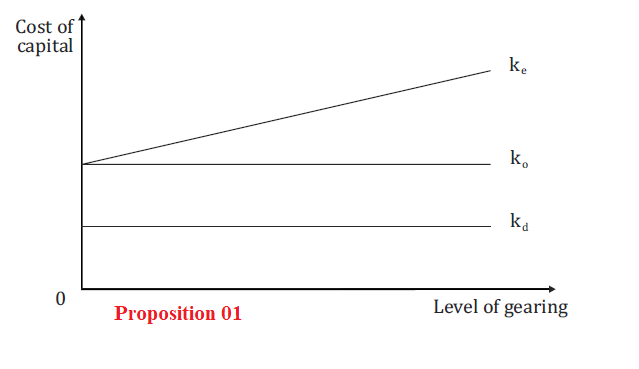

Proposition 01

In this situation cost of debt will rise because of increasing the gearing. However, the cost of equity increases to keep the WACC ( weighted Average Cost of Capital) at a constant.

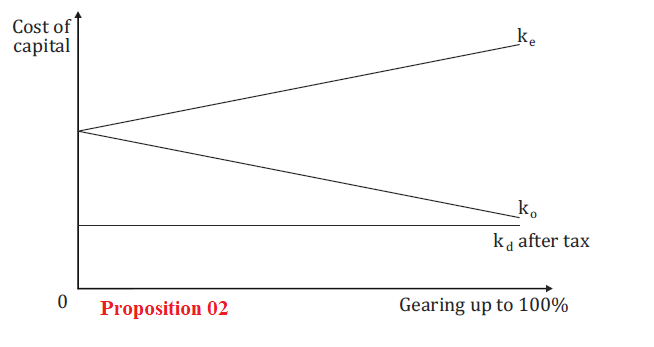

Proposition 02

In the previous proposition, we concluded that debt has no benefit in the absence of taxation. Therefore, in proposition 02 allowed MM to demonstrate that debt can be beneficial where tax relief applies. When the company increases its debt capital, tax relief on interest payments makes debt capital cheaper to a company, reducing the weighted average cost of capital.

Formulae and MM’s theory

Vg = Vu + TB

Vg = value of debt plus equity in a geared company

Vu = value of equity in an equivalent ungeared company

TB = tax shield on debt (T is the corporate tax rate and B is the market value of the geared company’s debt)

Weaknesses in MM’s theory

- MM assumes capital markets are perfect.

- MM ignored the higher financial distress cost and agency problem.

- It is Assumed that the investors act rationally and also ignored the transaction costs.

Capital structure in the real world

In the real world, some of the theories mentioned in the MM theories don’t exist. The most unrealistic is that perfect capital markets exist and that debt is

risk-free. Therefore, every lender has a greater risk, the same as the borrowers where there is a high level of gearing.

We can identify that several factors influence the capital structure of the company.

- Debt capacity

- Debt covenants

- Increasing debt costs

- Tax exhaustion – This is a situation where any further debt will not benefit from tax relief. Further elaborating, when gearing increases the interest portion will also increase. To obtain tax benefits, you need to have a taxable profit. If the taxable profits reached zero due to a more significant part of interest cost, the company would not be able to get further benefit from increasing gearing.

Let’s look for a particle situation where the capital structure theory will apply.

If you come across a newly started (young company), cash flows are always volatile, and Tax benefits < financial distress costs. Therefore, consider low gearing.

If you come across with a mature company, cash flows are stable and Tax benefits > financial distress costs. Therefore, consider increasing the gearing level.

Alternative theories of capital structure decisions

Static trade-off theory

This theory describes a situation where the firm will seek to a target level of gearing.

However, there are two financial distress costs faced by a firm.

- Direct financial distress costs

- Indirect financial distress costs

Direct financial distress costs

These are legal and administrative costs associated with the bankruptcy due to the higher gearing of the company.

Indirect financial distress costs

These are some of the implicit costs when the company faces a financial distress situation. E.g., High cost of capital, loss of sales, closing down plants, downsizing,

One of the main drawbacks of MM theory is that it ignores the existence of

financial distress costs. Therefore, when deciding the value of a geared company, the financial distress cost should be considered.

Value of a geared company – Value of the ungeared firm + present value of tax savings due to interest payments – the present value of financial distress costs.

Agency theory

We have already discussed this concept in earlier articles as well.

Agency costs of debt

When the company’s gearing increases, the probability of default also increases. If the company defaults in the future, shareholders can gain at the expense of debt holders. This could happen when the company decided to restructure its assets after the debt issue. If everything works out well as expected, the shareholder will gain the most out of it, but if it not, the loss will fall on the bondholders (Debt Holders).

Agency costs of equity

This agency cost is relating to the new share issue. This happens due to a conflict between old shareholders and new shareholders. New shareholders do not want the existing shareholders to benefit at their expense. Therefore, new shareholders will have to make mechanisms to monitor these things. However, the monitoring mechanisms are expensive, and the agency costs associated with the issue of new equity is increased with the amount of new equity issued.

Pecking order theory

This theory emphasizes the matter that the shareholders have less information than the directors of the company. Therefore, when shareholders are making a decision, they always consider the company director’s action.

Debt or equity?

As a rational finance manager, when you are deciding to finance the company using debt or equity, it is always probable that you pick the benefit one for your company. For instance, you would prefer to issue equity when the share price is high. Also, you would prefer to issue debt when the share price is low. Therefore, investors use the issue of equity/debt as the signal from managers about the worth of the shares.

Market signals

Assume a situation where a company started to issue equity shares. If so, then this will signal that stocks are overvalued. This may result in investors selling their shares, which will lead to a fall in the share price. Ultimately this will result in a higher cost of equity. However, as a manager, you should look for these consequences and consider issuing both debt and equity to avoid such adverse effects.

What is the preferred ‘pecking order” source of financing?

- Retained earnings

- Debt

- Equity

Adjusted present value (APV)

We have seen that the company’s gearing level has implications for its weighted average cost of capital (WACC). The APV system developed provides a better way to take into account the impact of using loan financing than a simple NPV analysis.

When to use the APV method

- The project uses subsidized loans

- The debt capacity is increasing

- Even to compare different capital structure options

APV calculations

There are only two steps of calculating the APV.

- Step 1 – Evaluate the project first as if it was all equity financed

- Step 2 – Allow the effect of financing

Other elements in APV calculation

Issue costs – This cost is also considered in APV calculations

Tax effect = Tax rate x Issue costs x Discount rate

Spare debt capacity – Increased borrowing or debt capacity should include in the APV calculations.

The present value of tax shield = Increased debt capacity x Interest rate x Tax rate x Discount factor

Subsidy – Sometimes, companies can obtain loans/debt at a cheaper rate than the normal rate. In this situation, you have to include in the APV calculation the tax shield effect of the cheaper finance and the effect of the saving in interest.

The advantages of the APV method

- This method will evaluate all the effects of financing – Tax shield, Changing capital structure, Any other relevant cost

- When using APV, you do not have to adjust the WACC using assumptions of perpetual risk-free debt.

The disadvantages of the APV method

- Difficulties in establishing a suitable cost of equity

- Identifying all the costs relating to the method of financing

- When deciding the relevant discount rates used to discount the costs

{kind=link}