Valuation of bonds

Bonds are a vital source of financing for businesses and governments. Therefore, valuation of bonds takes place a necessary role for the finance manager. This article begins with a description of the characteristics of the bonds and the explanation of the parameters. It then describes how to estimate bonds and calculate yield to maturity, thereby using cash discounts and time value knowledge. Then we will go through how the value of a bond can change over its lifetime and what happens if the market price of a bond does not reflect its value. Finally, let us discuss the time period, which is the average time it takes for the cash flow of an investor’s bonds.

Characteristics of bonds

Bonds

Bonds are long term financing methods. These have a nominal value, which represents the value owed by the company. There is also a coupon that represents the interest rate. For instance, if the company has issued 20% coupon bonds valued at $100, the interest value is $20. Bonds often issued at the par value. The coupon rate a fixed charged on the par value, and this doesn’t fluctuate whenever the market price of the bonds is changed. Besides, bonds usually redeemed at “par” value, but sometimes the redemption happens at a premium or discount price to that of nominal value “Par”.

Deep discount bonds

Deep discount bonds are offered at a significant discount rate to the nominal value. Therefore, investors likely to take advantage of the bonds through capital gains. So, the main characteristics of these types of bonds are larger discounts and lower Coupon rate.

Example of a deep discount bond

Assume a company issues $200000 value worth bond each at $40 in 2020. This would be redeemable in 2028 at $90. The capital gain, which will benefit from the investor, may be taxed at once.

Zero-coupon bonds

These types of bonds will not provide any interest “coupon” on the nominal value. However, investors gain through capital gains. The borrower will benefit from raising immediate cash. So, there is no cash payment until the redemption date. Therefore, the borrower can improve the financial health of the company until then. However, the redemption would depend on two factors,

- How much cash available

- The nominal rate of interest on debt

Valuation of bonds

The value of a bond is calculated using the present value of future expected earnings. As a finance manager/ student, you should keep in mind this golden rule when valuing any company’s financial asset/liability.

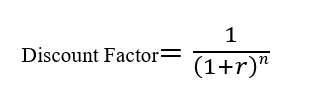

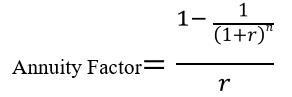

Valuation of redeemable bonds formula

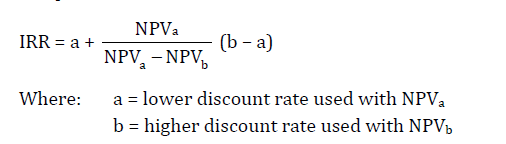

Yield to maturity

YTM is the effective yield of a redeemable bond after allowing for the time value of money. Similarly, YTM is also known as the return that investors required. YTM can be calculated using the IRR calculation.

Yield to maturity formula

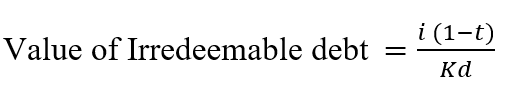

Valuation of irredeemable bonds formula

As far as the irredeemable bonds are concerned, the only cash flow will be the interest rate. Therefore, we can calculate the irredeemable bond value using the present value of future interest rates.

Valuation of irredeemable bonds formula

YTM – irredeemable bonds

Bond values and market prices

Market Prices of a bond

The value of a bond is determined by taking the present value of future cash flows discounting from the required yield for the debt. However, bonds are traded on the market, and the bond price depends on the supply and the demand factor. For instance, If the market price of a bond is less than its value, this will be an excellent opportunity to buy the bonds. In the long term, the investor expects the current market price to move towards the bond’s actual value. If that happens, investor would earn a profit.

Golden rule – There is an inverse relationship between bond price and yield.

How are bond prices determined?

Several factors determine the price of a bond. To understand these factors easily, we recommend you to go through each point with a redeemable bond value calculation.

- Required yield – As previously mentioned, then yield is higher price of a bond will reduce. Vice versa.

- Coupon – Higher the coupon, higher the bond value would be

- Redemption value – Most of the time, bonds are redeemed at “Par”. Sometimes it may be premium to par or discount to par.

- Time to maturity – When the bonds moving towards maturity, bond value will be more or less equal to redemption. However, in detailed explanation is given at the duration paragraph.

Moreover, the bond’s value should be similar to the par value of the bond when the following conditions are met.

- The bond will be redeemed at par

- The coupon rate = the required yield

- A coupon has just been paid

Similarly, bonds are valued at premium or discount to the par value due to these conditions.

- Bonds valued at a discount – When the required yield is higher than the coupon.

- Bonds valued at a premium – When the required yield is lower than the coupon.

Duration

Duration is also known as Macaulay duration. This shows the weighted average length of time to the receipt of a bond’s benefits. i.e. coupon and the redemption value. In other words, this time represents the time taken to recover the investment on the bond. Therefore, duration helps to compare bonds with different maturities and coupon rates.

Properties of duration

The primary characteristics of the sensitivity to interest rate risk are all reflected in the duration.

- Longer-dated bonds – Longer duration lower-coupon bonds – Longer duration

- Lower yields – Longer duration

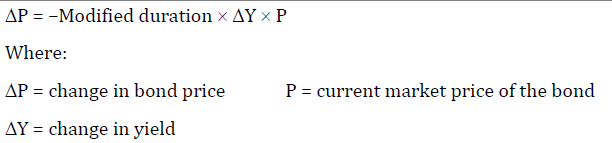

Modified duration

MD is a measure of the sensitivity of the bond price to a change in interest rates.

Modified duration formula

The above formula can be used to measure the bond price change to a given change in the yield.

You always need to remember that there is an inverse relationship exist between yield and the bond price.

Benefits of duration

- Duration allows us to compare bonds with different maturities and different coupon rates.

- As a finance manager, you can quickly determine the changes in the portfolio value based on the changes in interest rates.

- Managers can modify the interest rate risk by changing the duration of the bonds.

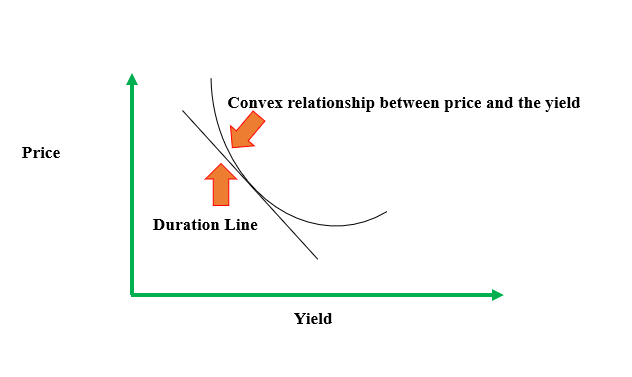

Limitations of duration

- It assumes that a linear relationship exists between bond price and interest rate, which is not valid. It will have a convex relationship between the price and the interest rate.

Credit risk

Credit risk is also known as default risk. Therefore, this implies the risk of being defaulted in interest and principal payments. There two factors which determine the credit risk of individual loan or bond.

- The probability of default – This is the probability where the borrower or counter party will default on its contractual obligations.

- The recovery rate – Even though a company may default on their payments, bondholders will never lose their entire amounts. Still, some parts of the owed amount can be covered. So, this represents the portion that can be recovered.

Loss given default

This is the difference between amount owed and the amount recovered.

LGD = Amount Owed – Recovered

Expected loss

Expected loss shows how much money lenders will lose from the investment made for the company as a bond or loan.

ES = LGD x Probability of default

Credit risk measurement

Calculating the credit risk for a company is hard. However, the companies’ credit rating is done by renowned credit rating companies such as Standard & Poor, Moody’s Investor Services, and Fitch.

What are the criteria for establishing credit ratings?

Following criteria will be taken when establishing credit ratings by the international firms,

- Country risk

- Industry risk

- Industry position

- Management evaluation

- Accounting quality

- Earnings protections

- Financial gearing

- Cashflow adequacy

Credit migration

The credit rating of a borrower may change after a bond is issued. This is simply called as credit migration. Due to the changing economic conditions or management decisions, borrowers may become more or less risky than when the bond was issued. Therefore, credit rating agency may issue a different credit rating for that particular company.

Reducing credit risk – credit enhancement

Credit enhancement is a method of reducing the credit risk of the company. This process is requiring collateral, insurance, or other agreements to reassure the lender that it will be compensated if the borrower defaulted. However, there are two types of credit enhancement methods.

Internal credit enhancement

Excess spread

This is also referred to as “excess interest cash flow “. The excess spread will calculate using the difference between interest received by issuers of asset-based securities (such as mortgages) on the securities sold and the interest paid to the holders of these securities.

Over-collateralization

In simple terms, it is the ratio of assets to liabilities. However, over-collateralization occurs when the ratio of assets to liabilities is greater than 1.

External credit enhancement

Surety bond

There are three parties involve in these types of agreement: Contractor (Company), Employer (Bond Holder), and the Guarantor. A surety bond is a guarantee to pay loss because of a breach of the agreement.

Letter of credit

Letter of credit most often used in international trade. A letter of credit represents a written promise made by a bank on behalf of the importer to pay the exporter a certain amount of time. However, to be eligible for payment, the exporter must be able to produce the documents that comply with the terms of the letter of credit.

Cash collateral account

A cash collateral account is an account that is used to secure and service a loan. This account is a kind of non-withdrawal type account, and it is viewed as a zero-balance account – any money that is paid in goes immediately towards reducing the extent of the loan being served.

Credit spreads

Credit spread is the premium required by the investors for facing the credit risk. Therefore, when calculating the required yield for investment in bond, both credit risk and the risk-free interest rate (Government Bond / US Government Treasury Bills) will be taken as a whole. We can calculated the credit spread using the below formula,

yield on corporate bond = risk-free rate + credit spread

Besides, there is an inverse relationship between credit risk and the credit spread. When the bonds have low credit quality, it will be attached with a high spread. Vice versa.

The cost of debt capital

Cost of the debt is determined using the following factors,

- Company credit rating

- The maturity of the debt

- Tax-free rate

- Corporate tax rate

Question

Seyloc Inc, a BBB rated company, has five-year bonds in issue. The current yield on equivalent US government bonds is 4.7%, and the current tax rate is 21%. Credit Spread is 1.27%

Required

Using the information stated above, calculate:

- The expected yield on Seyloc Inc’s bonds

- Seyloc Inc’s post-tax cost of debt associated with these five-year bonds

Answer

- Expected yield on five-year bonds = 4.7% + 1.27% = 5.97%

- Post-tax cost of debt = (1 – 0.21) x 5.97 = 4.72%

The impact of credit spreads on bond values

As we have previously mentioned, deterioration of the credit quality of a bond referred to as credit migration. Therefore, credit migration will reflect the increased spread. Similarly, there is also an impact on bond valuation as a result of credit migration.

{kind=link}